Liquid assets include cash and other assets that can quickly be turned into cash without losing value. You always want some of your assets to be liquid to cover living expenses and potential emergencies. But in a larger sense, think of liquidity as a spectrum: Some assets are more readily convertible into cash than others. At the far end of the spectrum are illiquid assets, which are very hard to value and sell for cash.

What Is Liquidity?

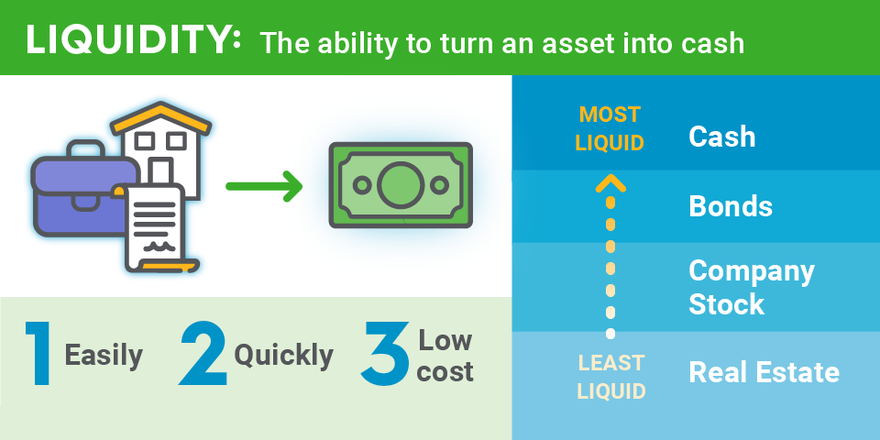

Liquidity describes your ability to exchange an asset for cash. The easier it is to convert an asset into cash, the more liquid it is. And cash is generally considered the most liquid asset. Cash in a bank or credit union account can be easily accessed via a bank transfer or an ATM withdrawal.

Liquidity is significant because owning liquid assets allows you to pay for basic living expenses and handle emergencies when they arise. But it’s important to recognize that liquidity and holding liquid assets come at a cost.

In general, the more liquid an asset is, the less its value will increase over time. Completely liquid assets, like cash, may even fall victim to inflation, the gradual decrease in purchasing power over time.

To protect against inflation and save for long-term financial goals, you’ll probably want to sacrifice some liquidity and lock assets into investments that grow your wealth over time, like investment securities or real estate.

But assets like real estate, art, and jewelry may be considered highly illiquid. This doesn’t mean you will never receive cash for them; it can be more challenging to value assets like this and turn them into cash.

What Are Liquid Assets?

Liquid assets are assets that can easily be exchanged for cash. While assets are valuable possessions that can be converted into cash, not all of your assets can be sold for cash right now or without a loss on the sale. Common liquid assets include:

- Cash. Cash is the ultimate liquid asset. Besides holding physical currency and ATM withdrawals, cash can be accessed via your checking account and peer-to-peer payment apps.

- Treasury bills and treasury bonds. T-bills and T-bonds are highly stable—and highly liquid—investments, backed by the full faith and credit of the United States government. Consequently, they can instantly be sold for cash on the secondary market if you need their value before they mature.

- Certificates of deposit. CDs can earn you higher APYs than checking or savings accounts but have stricter withdrawal restrictions. To access the money held in a CD before its maturity date, you may have to pay the penalty, typically a few months of interest. No-penalty CDs are an exception here, and they earn lower APYs.

- Bonds. Some investors buy bonds and hold them to their maturity date. But the secondary market for trading bonds is vast, meaning that many types of bonds are relatively liquid investments. Like any security, you may end up selling bonds for less than you paid for them.

- Stocks. Equities may be sold on stock exchanges almost instantly, and publicly traded stocks are considered very liquid. You usually receive cash from the sale within a few days. As noted above, you may sell a security-like stock for less than you paid for it.

- Exchange-traded funds (ETFs). ETFs are investment funds that trade like stocks on public exchanges, making them reasonably easy to sell quickly. While they are less risky than individual stocks and bonds, you may still have to sell ETFs at a loss if you need your money quickly. You will generally receive cash within a few days.

- Mutual funds. While they provide easy diversification, mutual funds only trade once daily, at the market close. This makes them slightly less liquid than stocks and ETFs. You generally receive proceeds from a sale the next business day.

- Money market funds. Money market funds are mutual funds that only own highly liquid assets, like cash, CDs, and government-backed debt. Because their components are highly liquid, their value is highly stable. Like mutual funds, you generally receive sales proceeds the next business day.

- Precious metals. Precious metals can be both liquid and illiquid. In some states, particular gold and silver coins can be used as currency, meaning it’s hypothetically as liquid as cash. Physical precious metals can also be exchanged for cash via dealers. But depending on where you store your precious metals, they may be less accessible.

Liquidity and Your Financial Accounts

Beyond individual asset classes, you should also understand the liquidity offered by the different accounts where you hold your assets. Certain account types are more liquid than others:

- Checking accounts. Checking accounts are the closest to cash in terms of liquidity. You can pay for things directly with a debit card, write a check, or withdraw cash.

- Savings accounts. Everyone should maintain both a checking account and a savings account, but it’s essential to understand that savings accounts are slightly less liquid. Federal rules prevent more than six convenient monthly withdrawals to encourage less frequent transactions. You can get around this limitation by conducting in-person transactions, mail, or ATM.

- Money market accounts. Another form of savings deposit, a money market account, may offer higher interest than a savings account and features such as using a debit card or check-writing privileges.

- Cash management accounts. Cash management accounts generally offer the liquidity benefits of checking accounts with higher interest rates at or above the levels of savings accounts. Because they aren’t savings deposits, they aren’t governed by the same withdrawal limitations. You should understand that some cash management accounts have low daily or monthly withdrawal limits, making them less liquid.

- Taxable investment accounts. These investment accounts are available via brokerages and are designed to hold stocks, bonds, ETFs, and mutual funds. They are pretty liquid, and when you sell assets held in a brokerage account, cash proceeds are transferred to your account within days of a sale. However, there’s a big potential downside: Depending on market conditions, you may have to sell your investment assets at a loss and incur trading commissions or sales fees.

- Tax-advantaged accounts. Tax-advantaged accounts, like your 401(k), individual retirement account (IRA), or health savings account (HSA), are less liquid than taxable investment accounts. They may hold similar investment assets, but their preferential tax treatment comes with significant limitations, such as penalties for their use before retirement or when they are used for non-qualified purposes.

- Trusts. Trust accounts can be reasonably liquid, depending on how they’re set up and managed. However, some trust structures are designed to make it harder to access and control the assets, so consult a trust attorney before setting up this account.

What Are Illiquid Assets?

Illiquid assets are not quickly sold or converted into cash. Some examples of illiquid assets include:

- Real estate. It can take weeks or months—or even years—to sell real estate. While it’s possible to access the equity, you have built up in a home or an investment property through a home equity loan, home equity line of credit, or a reverse mortgage, setting up these arrangements takes time and effort.

- Collectibles. Antiques, artwork, baseball cards, jewelry, and other collectibles can be challenging to value and hard to sell.

- Stock options. Many companies—not just tech start-ups—offer their employees stock options as a larger compensation package. Typically a new employee is promised a set amount of stock in the company that employs them if they remain with the company for a given period. Stock options can be precious, but they are highly illiquid assets, as you must remain with the company for years before you own the stock promised to you.

- Private equity. If you can invest in private equity assets, like venture capital or funds of funds, you have the potential to achieve significant gains. However, private equity funds often have steep restrictions on when you can sell your shares.

- Estates. Before you can access the assets in an estate, debts must be paid and taxes assessed. It can take years to benefit from an estate fully.

- Intangible assets. Intangible assets are concepts or ideas that have value—sometimes, a great deal of value. Intangible assets include corporate goodwill, brand recognition, intellectual property, and reputation. It can be challenging to assign a market value to intangible assets, which are, by nature, extremely illiquid.