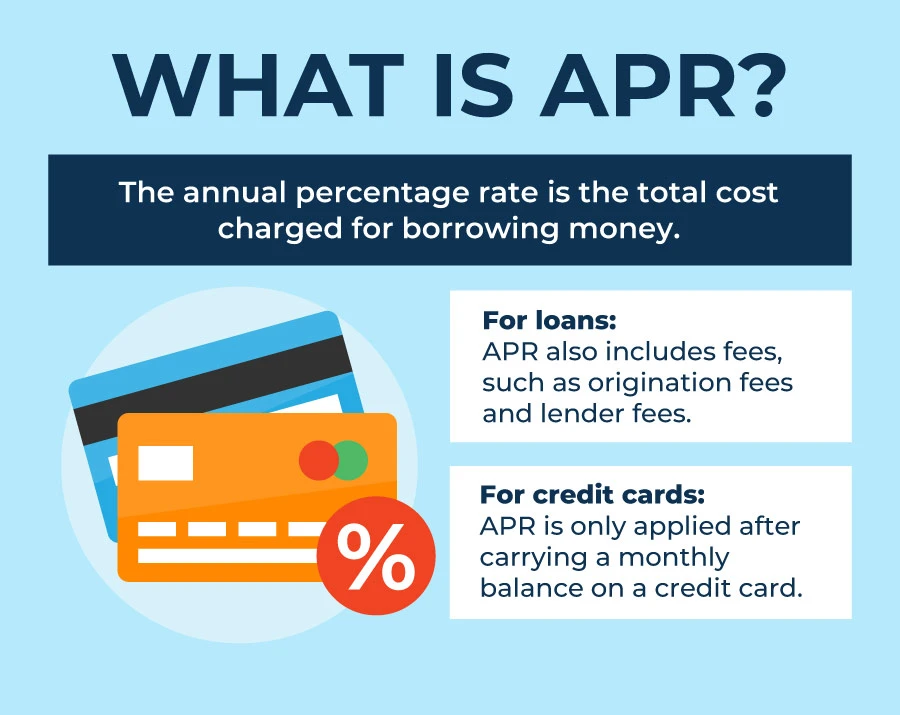

What Is Annual Percentage Rate (APR)?

Annual percentage rate (APR) refers to the yearly interest generated by a sum that’s charged to borrowers or paid to investors. APR is expressed as a percentage representing the actual yearly cost of funds over the term of a loan or income earned on an investment. This includes any fees or additional costs associated with the transaction but does not consider compounding. The APR provides consumers with a bottom-line number they can compare among lenders, credit cards, or investment products.

KEY TAKEAWAYS

- An annual percentage rate (APR) is the yearly rate charged for a loan or earned by an investment.

- Financial institutions must disclose a financial instrument’s APR before signing any agreement.

- The APR provides a consistent basis for presenting annual interest rate information to protect consumers from misleading advertising.

- An APR may not reflect the actual cost of borrowing because lenders have a fair amount of leeway in calculating it, excluding specific fees.

- APR shouldn’t be confused with APY (annual percentage yield), a calculation considering interest compounding.

How the Annual Percentage Rate (APR) Works

An annual percentage rate is expressed as an interest rate. It calculates what percentage of the principal you’ll pay each year by considering things such as monthly payments and fees. APR is also the annual interest rate paid on investments without accounting for interest compounding within that year.

The Truth in Lending Act (TILA) of 1968 mandates that lenders disclose the APR they charge to borrowers.1 Credit card companies are allowed to advertise interest rates monthly, but they must clearly report the APR to customers before signing an agreement.2

IMPORTANT

- Credit card companies can increase your interest rate for new purchases but not existing balances if they give you 45 days’ notice first.3

How Is APR Calculated?

APR is calculated by multiplying the periodic interest rate by the number of periods in a year in which it was applied. It does not indicate how often the rate is applied to the balance.

Types of APRs

Credit card APRs vary based on the type of charge. The credit card issuer may charge one APR for purchases, another for cash advances, and yet another for balance transfers from another card. Issuers also charge high-rate penalty APRs to customers for late payments or violating other cardholder agreement terms. There’s also the introductory APR—a low or 0% rate—with which many credit card companies try to entice new customers to sign up for a card.

Bank loans generally come with either fixed or variable APRs. A fixed APR loan has an interest rate that is guaranteed not to change during the life of the loan or credit facility. A variable APR loan has an interest rate that may change anytime.

The APR borrowers are charged also depends on their credit. The rates offered to those with excellent credit are significantly lower than those offered to those with bad credit.

WARNING

- APR does not consider interest compounding within a specific year: It is based only on simple interest.

APR vs. Annual Percentage Yield (APY)

Though an APR only accounts for simple interest, the annual percentage yield (APY) considers compound interest. As a result, a loan’s APY is higher than its APR. The higher the interest rate—and to a lesser extent, the smaller the compounding periods—the greater the difference between the APR and APY.

Imagine that a loan’s APR is 12%, and the loan compounds once a month. If an individual borrows $10,000, their monthly interest is 1% of the balance, or $100. That effectively increases the balance to $10,100. The following month, 1% interest is assessed on this amount, and the interest payment is $101, slightly higher than it was the previous month. If you carry that balance for the year, your effective interest rate becomes 12.68%. APY includes these small shifts in interest expenses due to compounding, while APR does not.

Here’s another way to look at it. Say you compare an investment that pays 5% per year with one that pays 5% monthly. For the first month, the APY equals 5%, the same as the APR. But for the second, the APY is 5.12%, reflecting the monthly compounding.

Given that an APR and a different APY can represent the same interest rate on a loan or financial product, lenders often emphasize the more flattering number, which is why the Truth in Savings Act of 1991 mandated both APR and APY disclosure in ads, contracts, and agreements.4 A bank will advertise a savings account’s APY in a large font and its corresponding APR in a smaller one, given that the former features a superficially larger number. The opposite happens when the bank acts as the lender and tries to convince its borrowers that it’s charging a low rate. A mortgage calculator is a great resource for comparing both APR and APY rates on a mortgage.

APR vs. APY Example

Let’s say that XYZ Corp. offers a credit card that levies interest of 0.06273% daily. Multiply that by 365, and that’s 22.9% per year, which is the advertised APR. Now, if you were to charge a different $1,000 item to your card every day and waited until the day after the due date (when the issuer started levying interest) to start making payments, you’d owe $1,000.6273 for each thing you bought.

To calculate the APY or effective annual interest rate—the more typical term for credit cards—add one (that represents the principal) and take that number to the power of the number of compounding periods in a year; subtract one from the result to get the percentage:

In this case, your APY or EAR would be 25.7%:

If you only carry a balance on your credit card for one month’s period, you will be charged the equivalent yearly rate of 22.9%. However, if you carry that balance for the year, your effective interest rate becomes 25.7% due to compounding daily.

APR vs. Nominal Interest Rate vs. Daily Periodic Rate

An APR tends to be higher than a loan’s nominal interest rate. That’s because the nominal interest rate doesn’t account for any other expense accrued by the borrower. The nominal rate may be lower on your mortgage if you don’t account for closing costs, insurance, and origination fees. If you roll these into your mortgage, your mortgage balance increases, as does your APR.

The daily periodic rate, on the other hand, is the interest charged on a loan’s balance on a daily basis—the APR divided by 365. Lenders and credit card providers are allowed to represent APR every month, though, as long as the full 12-month APR is listed somewhere before the agreement is signed.

Disadvantages of Annual Percentage Rate (APR)

The APR isn’t always an accurate reflection of the total cost of borrowing. In fact, it may understate the actual cost of a loan. That’s because the calculations assume long-term repayment schedules. The costs and fees are spread too thin with APR calculations for loans repaid faster or with shorter repayment periods. For instance, the average annual impact of mortgage closing costs is much smaller when those costs are assumed to have been spread over 30 years instead of seven to 10 years.

IMPORTANT

- Lenders have a fair amount of authority to determine how to calculate the APR, including or excluding different fees and charges.

APR also runs into some trouble with adjustable-rate mortgages (ARMs). Estimates always assume a constant rate of interest, and even though APR takes rate caps into consideration, the final number is still based on fixed rates. Because the interest rate on an ARM will change when the fixed-rate period is over, APR estimates can severely understate the actual borrowing costs if mortgage rates rise in the future.

Mortgage APRs may or may not include other charges, such as appraisals, titles, credit reports, applications, life insurance, attorneys and notaries, and document preparation. Other fees are deliberately excluded, including late fees and other one-time fees.

All this may make it difficult to compare similar products because the fees included or excluded differ from institution to institution. To accurately compare multiple offers, a potential borrower must determine which of these fees are included and, to be thorough, calculate APR using the nominal interest rate and other cost information.

Why Is the Annual Percentage Rate (APR) Disclosed?

Consumer protection laws require companies to disclose the APRs associated with their product offerings to prevent companies from misleading customers. For instance, if they were not required to disclose the APR, a company might advertise a low monthly interest rate while implying to customers that it was an annual rate. This could mislead customers into comparing a seemingly low monthly rate against a seemingly high annual one. Customers are presented with an “apples to apples” comparison by requiring all companies to disclose their APRs.

What Is a Good APR?

What counts as a “good” APR will depend on factors such as the market’s competing rates, the central bank’s prime interest rate, and the borrower’s credit score. When prime rates are low, companies in competitive industries will sometimes offer very low APRs on their credit products, such as 0% on car loans or lease options. Although these low rates might seem attractive, customers should verify whether these rates last for the full length of the product’s term or whether they are introductory rates that will revert to a higher APR after a certain period has passed. Moreover, low APRs may only be available to customers with especially high credit scores.

How Do You Calculate APR?

The formula for calculating APR is straightforward. It consists of multiplying the periodic interest rate by the number of periods in a year in which the rate is applied. The exact formula is as follows:

The Bottom Line

The APR is the basic theoretical cost or benefit of money loaned or borrowed. By calculating only the simple interest without periodic compounding, the APR gives borrowers and lenders a snapshot of how much interest they are earning or paying within a certain period of time. If someone borrows money, such as by using a credit card or applying for a mortgage, the APR can be misleading because it only presents the base number of what they are paying without taking time into the equation. Conversely, if someone is looking at the APR on a savings account, it doesn’t illustrate the full impact of interest earned over time.

APRs are often a selling point for different financial instruments, such as mortgages or credit cards. When choosing a tool with an APR, be careful also to consider the APY because it will prove a more accurate number for what you will pay or earn over time. Though the formula for your APR may stay the same, different financial institutions will include different fees in the principal balance. Be aware of what is included in your APR when signing any agreement.

- Federal Register. “Truth in Lending (Regulation Z).”

- Federal Trade Commission. “Truth in Lending Act.”

- Consumer Financial Protection Bureau. “When Can my Credit Card Company Increase my Interest Rate?“

- Federal Deposit Insurance Corporation. “Part 1030—Truth in Savings (Regulation DD).”

Note: ZPEnterprises is not a licensed investor/financial advisor, but we are trying to share awareness of financial topics. Please do further research and work with a licensed financial advisor.